Introduction

The management accountants’ provision to better inform themselves about management tools and techniques in management accounting. In this report, Pentland Group, renowned retail and wholesaler of fashion sportswear, accounting management tools and procedures have been discussed (Accountants, 2010).

The management sector in an organization that works with accounting provisions to make better managerial decisions that aids management functions and control organization performance is management accounting. Pentland Group has a management sector to manage its accounting aspects efficiently (Bhattacharyya, 2015).

Management accountant responsibility:

The managerial accountant of an organization holds the following responsibilities to perform his accounting management functions productively:

Fig: Roles played by a management accountant

Costing: The primary responsibility of an accountant is budgeting. Budgets guide a manager about the organization’s expenditures and to take investment decisions. For example, the management accountant of Pentland Group prepares accurate prediction of upcoming future costs and ensures business coordination reviewing the company’s historical data.

Decision-making: Management is provided with short-term and long-term decision-making information by a management accountant. The short-term decisions are optimum product mix, leasing, product pricing, etc. The long-term decisions are an investment, budgeting, financing, etc. For example, the accountant of Pentland Group chooses actions creditworthy for business after relevant analysis.

Planning: The management accountant makes analysis, budgets, and reports within a stipulated period to make valuable utilization of time. A timely forecast considers market uncertainties. According to available capital and market risk exposures planning accuracy is crucial. For example, the management accountant of Pentland group ensures the accuracy of information through proper planning before reporting the owners.

Control: A management accountant needs to be aware of situations that affect market competition, costs, inflation, raw material, coordination and other internal operations. An accountant should be able to control the situation being always ready for a cash crunch or any other risks. Informing the owners in advance the financial decisions can be made considering the fund availability and necessary supplies. For example, Pentland Group’s management accounting translates the specific objective and strategies through budgetary control and standard costing method.

Performance evaluation: A business is portrayed through the accounting system. Statements like Balance sheet and income statements report a business performance status. Management accounting directs business about profitability, performance, etc. For example, Pentland Group provides detailed analytical data to evaluate its performance.

Management accounting includes all the relevant information’s necessary for financial analysis and interpretation of operating activities. The part played by the magnitudes of management accounting within each business functions are demonstrated below (Bhimani, 2014):

| Scope | Relevance to a business function | Organizational Context |

| Cost accounting | The systematic procedure that records and reports cost measurements of manufacture and performance in details is cost accounting. Standard techniques applied in cost accounting are Marginal costing, Standard costing, Opportunity cost analysis, Differential cost, etc. | Pentland group analyses the opportunity cost to determine the next-highest value alternative for business growth. |

| Inventory management system | The software system that tracks the level of inventory, sales, order, and delivery is an Inventory management system. It monitors and maintains the business inventory sector. | Pentland Group uses the system to create a work order and bill of materials. |

| Inventory cost | The costs in association with storage, procurement and inventory management. Fee included in inventory costs are Order Cost, Carrying cost, Stock out the cost, etc. | Pentland Group determines Inventory cost before procuring goods that requires inventory management. |

| Job costing | The accounting system that tracks expenses and profits according to business roles is job costing. Data management relevant to business operations becomes flexible with this method. | Pentland Group tracks the cost of each job with its job costing. |

| Price optimizing system | The program that determines the relation of demand with different price levels, and combines data with expenses and inventory level to recommend prices that is profitable for the business is optimizing price system. | Pentland Group uses an optimizing price system to determine customers reaction to their service based on the price level. |

Differences between a management accountant and financial accountant

Management accountant and financial accountant are a major part of an organization’s financial sector. Both play their role in helping business growth through appropriate financial decision implementation. The differences amongst them are (Drury, 2017):

| Financial Accountant | Management Accountant |

| Definition | |

| Financial Accountant relates and provides information to people outside the organization. | Management Accountant relates and provides information to people within the organization. |

| Primary activity | |

| Primary activities are a daily financial transaction and determine organizations financial health. | The primary activity is to report financial information to management to make necessary business decisions. |

| Purpose | |

| The financial accountants’ activities are used for stakeholders to evaluate organizations financial performance. | The accountant managements activities are used for internal financial management, like making budgets. |

| Report format | |

| A standardized format needs to be followed as prescribed for the applicable act. | There is no standardized format of report as the internal body of the organization uses it. |

| Frequency | |

| Financial Accountant Prepares report based on statutory requirements: Monthly, Quarterly, yearly, etc. | There is no fixed interval of report preparation by a management accountant and prepares report whenever upper management demands. |

| Compliance | |

| A financial accountant is required to maintain the statutory compliance. | A management accountant need not required to maintain the statutory compliance. |

| Focus | |

| A financial accountant focuses on historical data while preparing a report within a fixed period. | A management accountant focuses on data presentation and forecasts future reports. |

| Set of skills | |

| A financial accountant is required to have a strong base on accounting standards, such as IFRS, GAAP, etc. | A management accountant requires good knowledge on an accounting basis, like, cost accounting, budget preparation, MIS, etc. |

| Certified Courses | |

| Following certified courses are mandatory for a financial accountant:Chartered Accountancy (CA)Association of Chartered Certified Accountants (ACCA)Chartered Public Accountants (CPA). | Following certified courses are mandatory for a management accountant:Chartered Institute of Management Accountant (CIMA)Cost and Management Accountants (CMA) |

| Example | |

| The financial accountant of Pentland Group makes financial statements. | The financial statement is used by the management accountant of Pentland Group to make budgetary decisions. |

Financial Accountant and Management Accountant overlapping disciplines.

The overlapping disciplines among financial accountant and management accountant are (Gill, 2014):

Accounting Information: Both the management accountant and financial accountant uses accounting information to provide business financial information. Even though the users of this information are different. For example, Pentland Group’s financial accountant provide information to creditors, while the management accountant provides information to the company managers using the same accounting guidelines.

Report Format: Both financial accountant and management accountant represents their analysis in a standard report format. Though the reports tend to differ, accounting principles regulate financial accounting reports while management accounting reports are not. For example, Financial accountant of Pentland Group follows GAAP standard in presenting a balance sheet or income statement that shows a company’s position within a specific period. The management accountant of Pentland Group reports on incurring costs according to the company’s prescribed format.

Educational Expertise: Management accounting and financial accounting are widely recognized field and typically requires accounting programs before an accountant receives a degree on that particular field. For example, Pentland Group HR seeks CPA for a financial accountant and CMA for managerial accountant.

Cost Reports

The reports that provide cost accounting information of a company with expenses and revenues in detail is cost reports. Different types of cost reports are explained with the cited example from Pentland Groups reports (Jain, 2016).

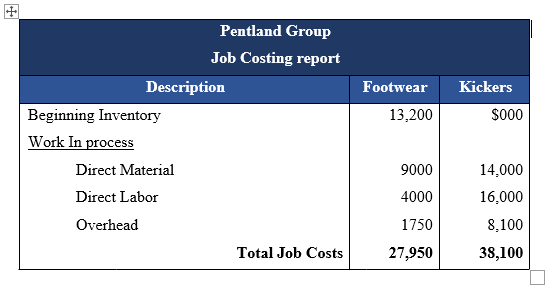

Job Costing report: The cost report that accumulates costs according to specific jobs using the job cost system to identify individual products to meet customer need is job costing report. A job costing report of Pentland Group is cited below:

Batch Costing: The costing report that shows the calculation of each batch cost is batch costing report. In this method, the price per unit is ascertained by dividing the total cost of the batch by numbers produced. Following batch cost sheet of Pentland Group is prepared:

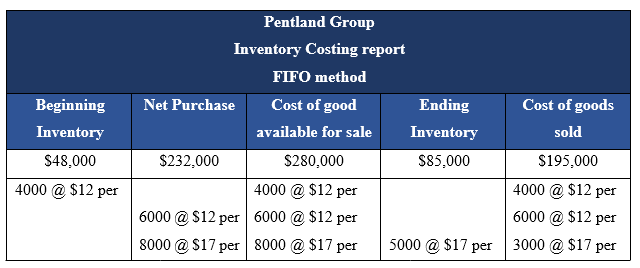

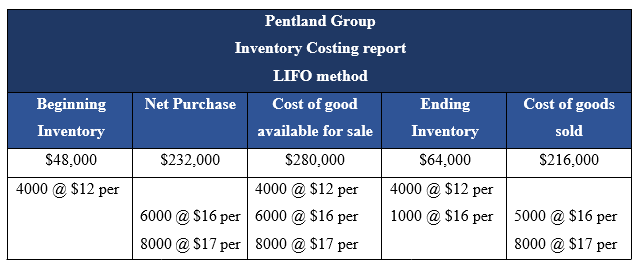

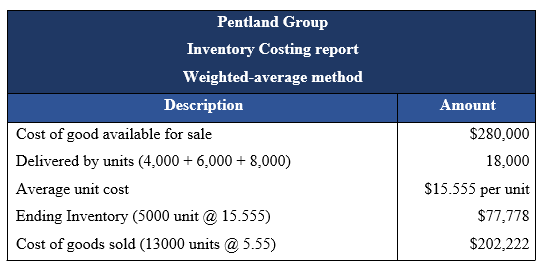

Inventory Costing: The cost report that shows the determination of inventory valuation. The three primary costing method are FIFO, LIFO and weighted average cost (Pandikumar, 2019).

First-in, First-out (FIFO) method assigns the most recent purchases in ending inventory. For Pentland Group, a FIFO method is applied for Sportswear.

Last-in, first-out (LIFO) method is inverse of FIFO method and sends out oldest inventory first. The LIFO method is applied for the same Sportwear of Pentland Group.

The weighted-average method applies the average unit cost to calculate total unit sold and ending inventory. For the same Sportwear of Pentland Group, the weighted average method is applied:

The differences among the inventory costing method are highlighted below:

Stock cost reduction: By organizing the warehouse, using consignment inventory and getting rid of obsolete stocks, the cost of capital can be reduced.

Activity-based costing is the costing report that identifies the cost activity to all product and services by actual consumption is activity-based costing report. This report assigns indirect costs into direct costs compared to traditional costing method (Prakashan, 2014).

Benefits of Cost reports:

| Cost Method | Benefits |

| Job Costing report | • The profit earned in specific jobs is calculated. • Forecasts whether specific jobs are desirable to pursue. |

| Batch Costing | Cheaper to produce the whole batch rather than individual productionEfficient use of machinesLow cost with few workers |

| Inventory Costing | • Control of cost is improved• Productive planning and decision-making• Saves costs through record-keeping |

| Activity-based costing | • Decisions made are much better• Traces cost object activities• Better cost management |

Differences among various cost report

| Basis | Job Costing | Batch Costing | Inventory Costing | Activity-based costing |

| Analyses costs of | Job | Batch of units | Inventory | Activity |

| Order of activity | Single | Stock | Total unit | Total unit |

| Other Reports | Business benefits | Helps is adding Organization value | Helps in organization goal attainment |

| Performance report | Improves customer insights | Addresses the outcome of business activity | Focuses on the best sales opportunity |

| Operating budget report | Makes sure the things are on track. | Shows a company’s expected earnings and expenditures. | Have the potential to attract investors towards the company. |

| Accounts receivable ageing report | Determines overdue. | Lists the unpaid customer invoices | Identifies customers falling behind payment |

| Job cost reports | The profitability of each job can be individually determined | Evaluate project performance | Motivates staff to increase their output level. |

| Inventory Management Reports | Directs for sensible purchases | Outline information about the current inventory level | Integrates entire business. |

The management accountant of Pentland Group is considering the sales of sportswear as determined by the financial accountant. From the stated analysis, an income statement of Marginal costing and Absorption costing is followed (Reddy, 2014).

Absorption costing techniques: The costing technique used to calculate product cost by considering indirect expenses along with direct expense. For Pentland Group, the absorption costing technique is applied below (SINGH, 2016):

Marginal costing techniques: The costing technique that includes the cost of additional inputs required to produce the next unit is minimal costing technique. For Pentland Group, the minimal costing technique is as below (SINGH, 2016):

The organization may use one technique over another

The difference between fixed and variable cost while profit calculation is not done in absorption costing method. Marginal cost techniques, on the contrary, show variable and fixed costs separately. For this reason, on necessity, the company may use one technology over another (Terence Lucey, 2013).

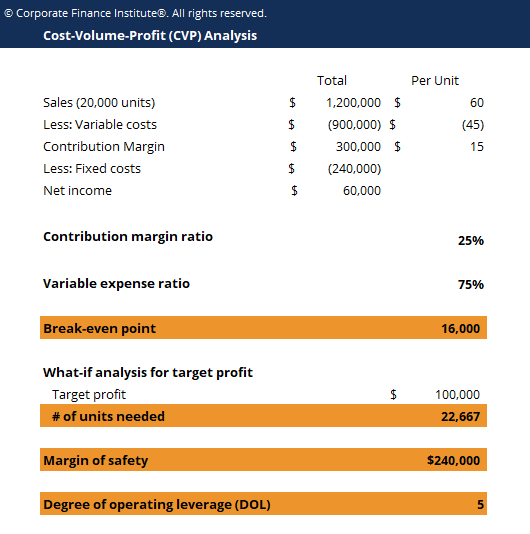

The point at which total revenue and total cost equal to each other refers to Break-Even Analysis. For Pentland Group, the fixed cost of sports shoe is determined by the managerial accountant who is $100,000. The variable cost is $2 per sports shoe. The selling price is $12. The break-even point of Pentlands is analyzed below (SINGH, 2016):

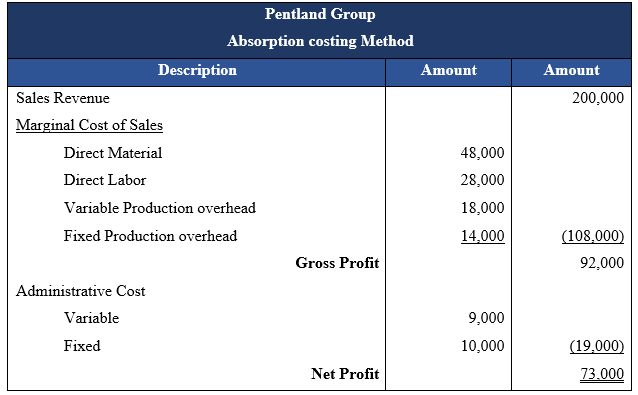

Break-even quantity

= Fixed Cost / (Selling Price –- variable cost)

= $100,000 / ($12 – $2)

= 10,000

Hence, Pentland needs to sell 10,000 units of sports shoe to reach the break-even.

Graphical Representation

The Break-even chart, also known as the Cost Volume Chart shows the example cited above:

Fig: Break-even Analysis

Therefore, the concept of break-even point is as follows:

Profit when Revenue > Total Variable cost + Total Fixed cost

Break-even point when Revenue = Total Variable cost + Total Fixed cost

Loss when Revenue < Total Variable cost + Total Fixed cost

Importance of Break-even: The cost structure can be determined using Break-even analysis as it shows the number of units to be sold to make a profit.

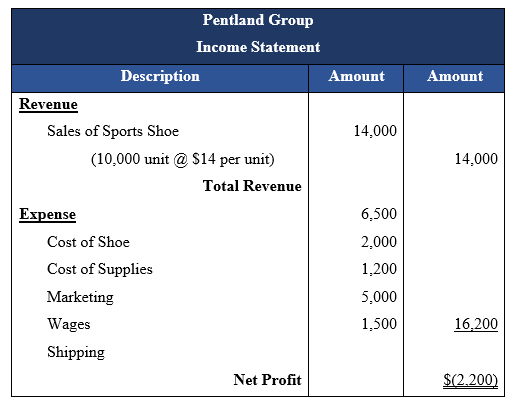

Net profit is the actual profit earned after all expensed. A net profit for Pentland Group sports shoe sell is determined below (Accountants, 2010):

.

Importance of Net Profit

Management accountant: A management accountant should know and give priority to net profit as it demonstrates business success.

Organization Objective fulfilment: The main objective of an organizational aim is profit generation. Net profit indicates the amount available to pay the owner and reinvest them.

Investment decision: There is no point of making too many sales which don’t generate profit. Net profit shows whether a sales decision should be made or not. The above example shows that investment should not be made for possible losses.

Conclusion

The report emphasis on the application of management accounting tools and techniques. It is recommended that the proper implementation of accounting tools can productively increase business performance (Bhimani, 2014).

References

Accountants, N. A. o., 2010. Management Accounting. 11th ed. s.l.: National Association of Accountants.

Bhattacharyya, D., 2015. Management Accounting. 8th ed. s.l.: Pearson Education India.

Bhimani, A., 2014. Contemporary Issues in Management Accounting. 7th ed. s.l.: Oxford University Press.

Drury, C., 2017. Management and Cost Accounting. 8th ed. s.l.: Cengage Learning EMEA.

Gill, S., 2014. Cost and Management Accounting: Fundamentals and its Applications. 6th ed. s.l.: Vikas Publishing House.

Jain, K. &., 2016. Management Accounting. 12th ed. s.l.: Tata McGraw-Hill Education.

Nandakumar, M. P., 2019. Management of Accounting theory and practice. 13th ed. s.l.: Excel Books India.

Prakashan, N., 2014. Management Accounting. 7th ed. s.l.: Nirali Prakashan.

Reddy, R., 2014. Management Accounting. 8th ed. s.l.: APH Publishing.

SINGH, S., 2016. MANAGEMENT ACCOUNTING. 5th ed. s.l.: PHI Learning Pvt. Ltd.

Terence Lucey, T. L., 2013. Management Accounting. 5th ed. s.l.: Cengage Learning EMEA.